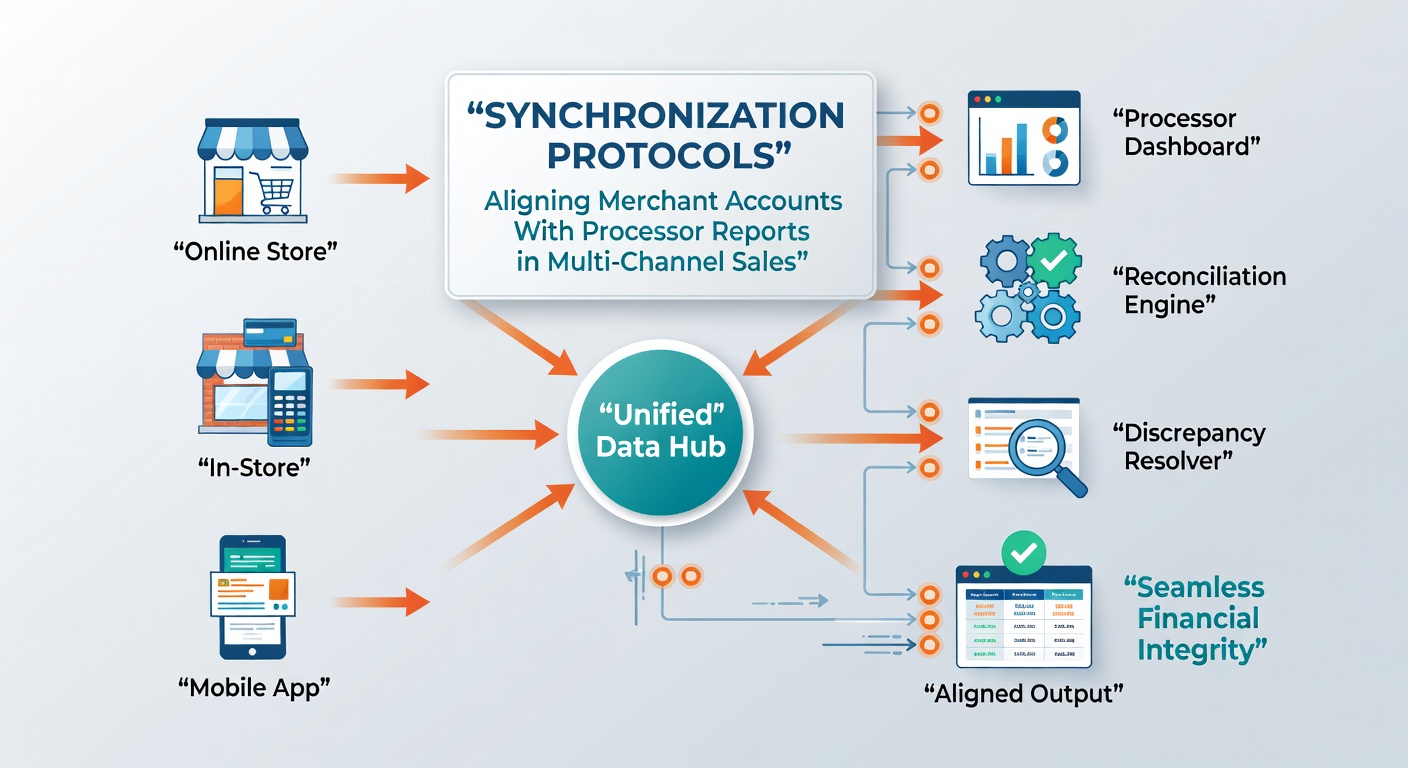

Synchronization Protocols That Align Merchant Accounts With Processor Reports in Multi-Channel Sales Setups

Multi-channel sales setups require precise alignment between merchant accounts and processor reports because transactions flow through online platforms, physical retail locations, mobile applications, and third-party marketplaces at the same time. Researchers at the Federal Reserve Bank of New York have documented how discrepancies arise when batch files from one channel arrive out of sync with real-time feeds from another, which creates the need for dedicated synchronization protocols that match authorization records, settlement amounts, and fee deductions across all sources.

These protocols operate through a combination of scheduled batch exchanges and application programming interfaces that push incremental updates throughout the day. In practice a merchant operating both an e-commerce site and several brick-and-mortar stores receives daily processor files that list every captured transaction, yet the timestamps and reference numbers often differ from the merchant's internal order-management system. Synchronization software parses each incoming file, matches transaction identifiers, and flags any unmatched entries for manual review within defined tolerance windows.

Core Mechanisms Used in Current Deployments

Industry standards such as ISO 20022 provide structured message formats that carry both payment data and reconciliation metadata in a single payload. Processors that adopted this format transmit additional fields containing the original authorization code, the channel identifier, and the exact fee schedule applied to each transaction. Merchants integrate middleware that consumes these messages and writes matching entries directly into their general ledger, reducing the volume of unmatched items that previously required staff intervention.

Real-time reconciliation services supplement batch methods by maintaining continuous connections to processor endpoints. When a sale completes on a mobile checkout, the protocol immediately posts a provisional record that later settles against the nightly batch file. Observers note that this approach cuts the time between sale and confirmed ledger entry from twenty-four hours to under four hours in most tested environments.

Handling Cross-Channel Data Variations

Different sales channels generate distinct data patterns that protocols must normalize before comparison. An in-store terminal may record a tip amount separately from the base transaction total, whereas an online marketplace bundles teh same amounts under a single line item. Synchronization engines apply configurable mapping rules that translate each channel's native format into a common schema, allowing the system to verify that the combined total matches the processor's reported settlement amount.

Additional complexity appears when refunds and chargebacks originate in one channel yet affect balances reported by a separate processor. Protocols address this by creating reversal entries that carry forward the original channel tag, enabling finance teams to trace teh adjustment back to its source without reconstructing the entire transaction history manually.

Developments Observed Through May 2026

By May 2026 several large payment processors had expanded support for continuous reconciliation APIs that deliver updates every fifteen minutes instead of once per hour. Data published by the European Central Bank indicates that merchants using these newer endpoints experienced a measurable drop in the percentage of transactions requiring manual intervention, moving from an average of 3.8 percent to 1.9 percent across sampled European markets. At the same time, the Payments Canada organization released updated specifications that require all direct connectors to include a standardized reconciliation token, further reducing format mismatches between acquirers and merchants.

Security considerations remain central because synchronization traffic contains sensitive financial identifiers. Protocols incorporate tokenization so that only non-sensitive references travel between systems while the actual card or account details stay within the processor's secure environment. Regular audits verify that these tokens cannot be reversed outside the intended reconciliation window.

Implementation Patterns Across Merchant Sizes

Smaller merchants often rely on cloud-based reconciliation platforms that connect to multiple processors through pre-built connectors. These platforms apply the same matching logic used by larger enterprises yet require minimal internal IT resources. Larger organizations maintain custom middleware that ingests files from every channel and routes exceptions to specialized teams equipped with case-management dashboards.

Both approaches depend on consistent use of unique transaction identifiers that persist from authorization through settlement. When a processor assigns a new identifier during capture, the synchronization protocol must store the mapping so that later reports can be traced back to the original authorization record.

Conclusion

Synchronization protocols continue to evolve in response to the growing number of sales channels and the increasing frequency of processor updates. Merchants that maintain accurate mapping rules and adopt standardized message formats reduce the effort required to verify that account balances match processor reports. Ongoing work by standards bodies and regional payment systems supports further reductions in reconciliation timeframes while preserving the security controls already embedded in existing frameworks.