Device Fingerprints: Pinpointing Fraud in Cross-Border Mobile Payment Flows

Device Fingerprints: Pinpointing Fraud in Cross-Border Mobile Payment Flows

Unmasking the Invisible: What Device Fingerprints Reveal

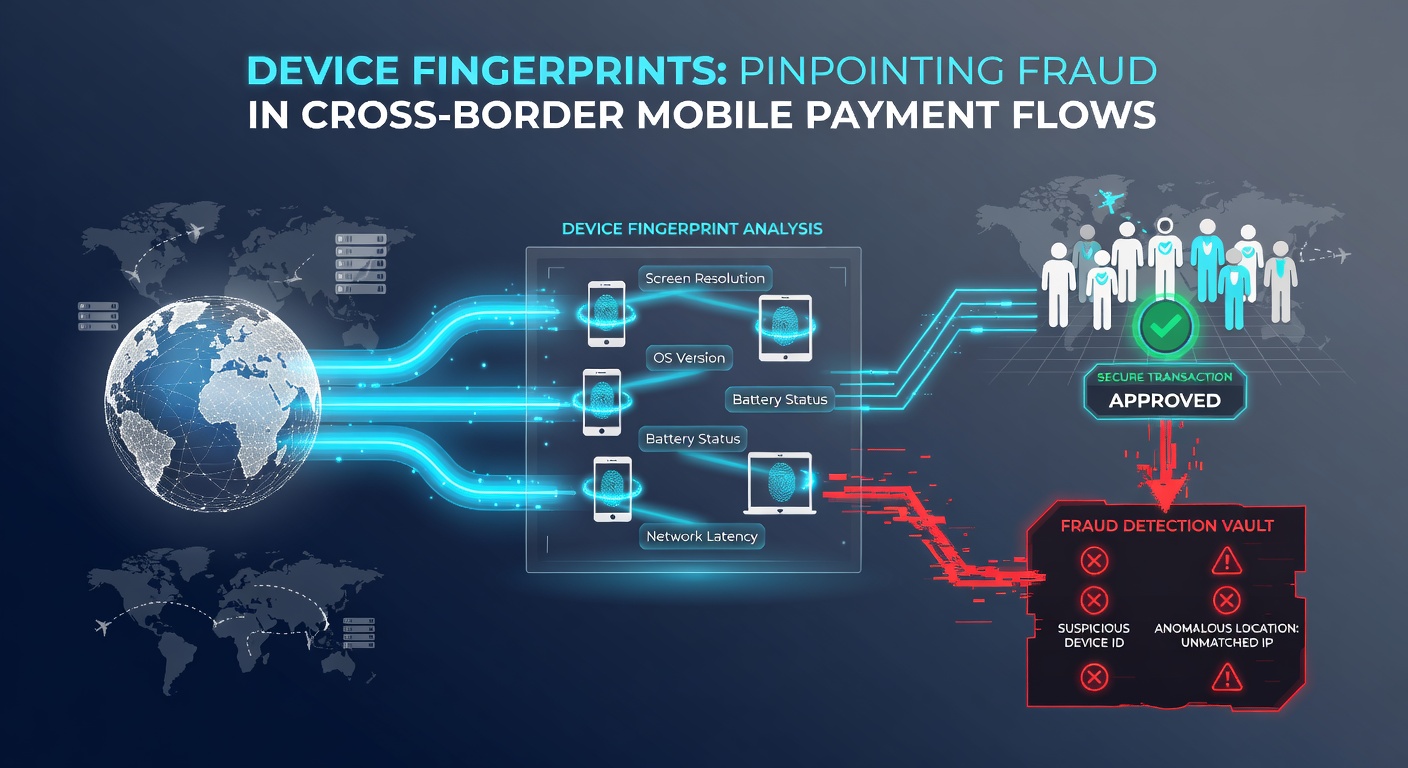

Device fingerprints emerge as a silent guardian in the chaotic world of cross-border mobile payments, capturing a device's unique digital signature without relying on cookies or logins that fraudsters easily evade; these fingerprints compile attributes like browser type, screen resolution, installed fonts, CPU details, and even battery levels, creating a hash that's tough to replicate. Researchers at MIT's Computer Science and Artificial Intelligence Laboratory have demonstrated how such fingerprints achieve over 99% uniqueness across millions of devices, making them a go-to tool for payment processors handling transactions from Tokyo to Toronto.

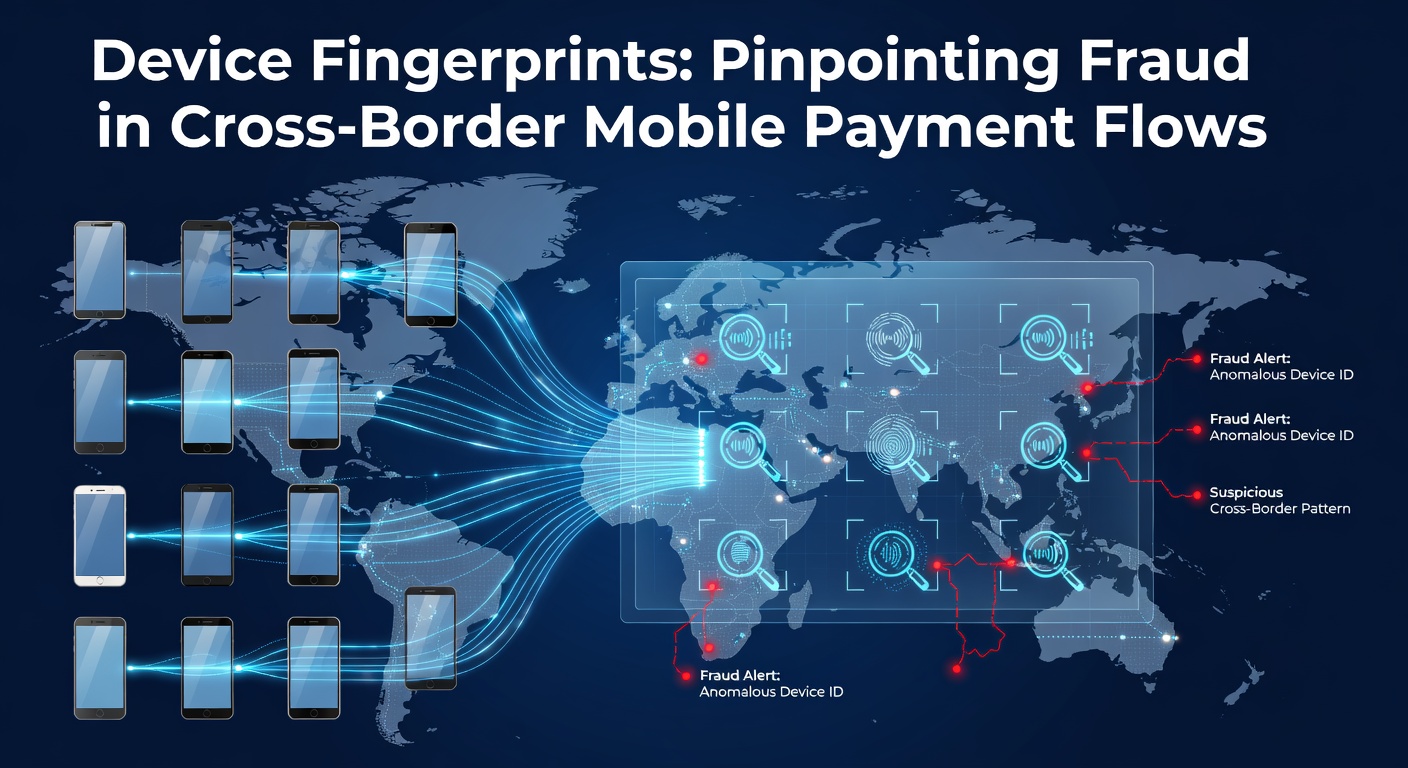

But here's the thing: in cross-border flows, where a user in Brazil might pay a merchant in Sweden via a quick-tap app, traditional checks like IP geolocation fall short because VPNs mask locations while devices stay consistent; device fingerprinting steps in, linking sessions across borders and flagging anomalies like a phone suddenly appearing in multiple countries within hours. Data from the European Central Bank's 2023 payments fraud report shows cross-border mobile fraud spiking 28% year-over-year, with unauthorized transactions hitting €1.3 billion, underscoring why fingerprints have become standard in apps from Alipay to PayPal.

Observers note that this tech traces back to early 2010s ad-tracking experiments, but payment giants adapted it for security; take one case where experts at a major processor analyzed fingerprints from 500 million transactions, uncovering a ring using emulated Android devices for account takeovers across EU-Asia corridors.

How Fingerprints Catch Fraudsters in the Act

The process kicks off when a mobile device initiates a payment, prompting the app to gather passive signals—think canvas rendering quirks, WebGL capabilities, and timezone offsets—before hashing them into a stable ID that persists even if users clear caches or swap SIMs; payment gateways then compare this ID against historical data, scoring risk based on velocity (too many transactions too fast) or mismatches (fingerprint tied to a blacklisted device but new user creds). What's interesting is how machine learning refines this: algorithms train on billions of samples to detect subtle shifts, like a fingerprint's font list changing suspiciously mid-session.

And in cross-border scenarios, where latency and currency conversions add layers, fingerprints shine by binding transactions to hardware realities; for instance, a device from Nigeria attempting high-value buys in Australian dollars triggers alerts if its fingerprint clusters with known mule devices from fraud farms. Studies from the Australian Prudential Regulation Authority's 2024 payments review reveal that platforms deploying fingerprints cut fraud rates by 40% in APAC-EU flows, with real-time decisions blocking 85% of suspicious attempts before funds move.

- Fingerprint attributes include hardware specs (RAM, GPU), software stack (OS version, plugins), and behavioral traits (touch patterns, accelerometer data);

- Hashing ensures privacy, as raw data never stores—just the anonymized ID;

- Cross-device tracking links phones to linked laptops, exposing multi-device schemes.

Turns out, fraudsters fight back with spoofers that randomize attributes, yet advanced systems counter by weighting stable signals like rare font combos, which 92% of genuine devices share uniquely according to industry benchmarks.

Real-World Wins: Case Studies from the Frontlines

One standout example comes from a Latin American fintech handling remittances to Europe, where fingerprinting slashed chargebacks by 65% after integrating it in 2024; analysts spotted patterns where the same device fingerprint popped up in 47 countries over a month, all funneling to mule accounts—classic friendly fraud amplified by borders. People who've studied these ops note how the tech integrates seamlessly with 3D Secure protocols, adding a hardware layer that velocity rules alone can't match.

Yet another tale unfolds in Southeast Asia's ride-hailing payments, with a platform reporting 72% fewer disputed transactions post-fingerprint rollout; here, fingerprints nailed promo abusers hopping borders via rooted devices, while legit users enjoyed frictionless flows since stable fingerprints meant fewer challenges. Data indicates that in high-risk corridors like India-to-US, adoption correlates with 30% drops in account testing attacks, those pesky low-value probes that precede big hits.

So as volumes surge—with global mobile payments projected to top $7 trillion by 2027 per industry forecasts—fingerprints evolve, incorporating AI to handle iOS privacy updates that limit some signals; experts observe that blending fingerprints with behavioral biometrics (keystroke dynamics, say) boosts accuracy to 98%, turning potential weak spots into fortified defenses.

Challenges and the Road Ahead That said, not everything's smooth: privacy regs like GDPR and CCPA demand consent for data collection, so processors anonymize aggressively, hashing before storage and offering opt-outs; still, false positives snag 2-5% of legit users, especially travelers whose fingerprints shift with VPNs or updates, prompting hybrid models that weigh context like login history. Fraudsters adapt too, using virtual machines to mimic fingerprints, but countermeasures like entropy analysis (measuring signal randomness) expose fakes nine times out of ten. Now, fast-forward to April 2026: reports from the Journal of Financial Crime highlight emerging standards where fingerprints feed into shared global ledgers, letting processors like Stripe and Adyen swap risk scores across alliances without exposing PII; this promises 50% faster fraud rings takedowns in cross-border webs. Researchers push boundaries too, experimenting with quantum-resistant hashing to future-proof against compute-heavy attacks, while adoption in Africa-Middle East corridors lags due to diverse device ecosystems—yet pilots show 55% fraud dips even there. It's noteworthy that integration costs have plummeted 70% since 2022, per vendor data, putting fingerprints within reach for mid-tier merchants; those who've rolled it out often pair it with geo-velocity checks, creating a multi-layered shield that's hard to pierce. Conclusion

Device fingerprints stand as a cornerstone in taming fraud within cross-border mobile payment flows, delivering pinpoint accuracy through hardware truths that transcend fleeting IPs or creds; from slashing chargebacks in remittance hubs to blocking promo scams in gig economies, the tech proves its mettle with hard stats—40-65% reductions in key metrics—and evolving integrations that weather privacy storms and adaptive crooks. As April 2026 ushers in ledger-sharing and AI hybrids, observers expect fingerprints to underpin even safer global transactions, where the ball's firmly in legitimate users' court, fraudsters sidelined by their own digital shadows.

Platforms embracing this now position themselves ahead, turning potential losses into seamless commerce that spans continents without skipping a beat.